How Disclosure of Loan Loss Provisions Contributes to Financial Stability

The financial crisis of 2007-2008 significantly impacted the economy and the population, underscoring the crucial role of a stable financial sector in facilitating diverse economic interactions. To promote a stable financial sector, the EU adopted numerous regulations, including stricter reporting requirements for loan loss provisions which increased the transparency of banks’ loan losses. As a result, privately-held banks in Germany, i.e., those without publicly traded shares or debt, were required to disclose their loss provisions in detail for the first time.

There are highly controversial views regarding the role of transparency in financial stability, particularly whether increased transparency increases the risk of downward spirals during a crisis or whether it disciplines managers’ risk-taking ex ante. In light of this debate, TRR 266 researcher Jannis Bischof, together with co-authors Daniel Foos and Jan Riepe, analyzed the effects of increased transparency on privately-held banks. Their findings suggest that financial stability benefits from greater transparency, as it disciplines bank managers’ risk-taking and reporting choices even in the absence of stock market pressure. The study “Does Greater Transparency Discipline the Loan Loss Provisioning of Privately Held Banks?” has been published in the European Accounting Review.

The global financial crisis of 2007-2008 was precipitated by the collapse of the real estate bubble in the USA, coupled with opaque banking transactions. It had a devastating impact on banks, companies, and numerous private individuals. Governments around the world intervened to bail out banks and prevent further economic collapse. Despite these efforts, millions of people suffered significant financial losses, and numerous companies faced the most severe crisis since the Great Depression. This underscored the critical importance of a stable financial sector for both businesses and individuals.

The majority of banks worldwide are not listed on any stock exchange and, therefore, lack any strong incentives for transparency. For example, these privately-held banks are rarely subject to the strict disclosure requirements of IFRS. They can more easily resist external pressures for greater transparency, as their shareholders typically have access to private information and do not rely on public financial reports. However, both the lack of transparency and the introduction of measures to promote transparency can lead to unforeseen consequences. Thus, it is crucial to understand the role of transparency in the reporting practices of privately-held banks and its broader implications. The study focuses on how the German implementation of an EU regulation on loan loss provisions affects bank transparency and whether increased transparency disciplines management behavior in the absence of stock market pressure.

What are loan loss provisions (LLP)?

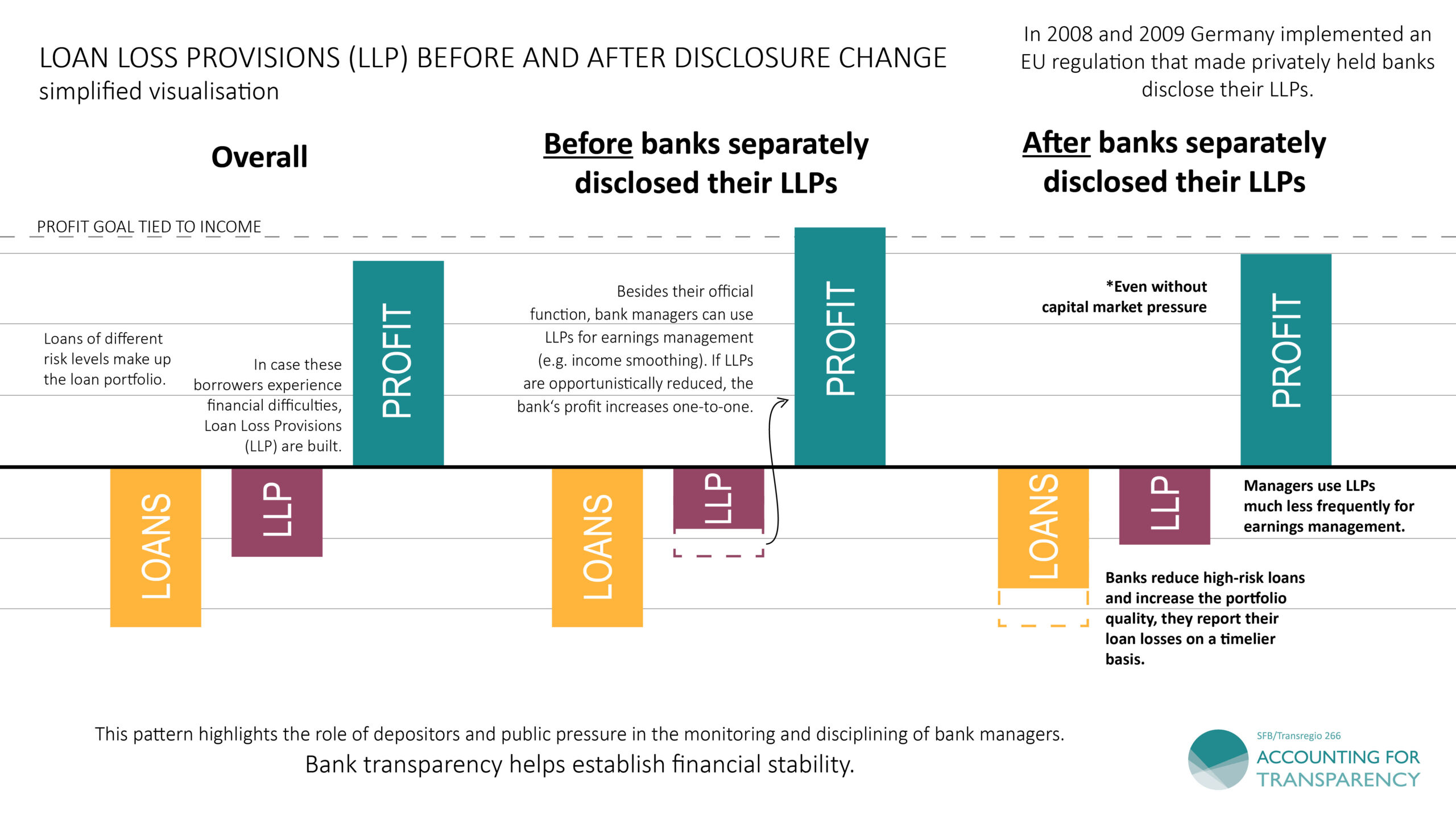

Whenever banks grant loans, they bear the risk that the loan will not be fully repaid. In response to this credit risk, banks charge higher interest rates based on the loan’s default risk and at the same time set aside funds as loan loss provisions (LLPs). Managers continuously adjust these LLPs for all active loans to adequately account for credit risk. Given the forward-looking nature of loan loss estimation and the inherent uncertainty about future loan defaults, bank managers have considerable discretion in determining what constitutes an “appropriate provision”. Too high a provision can make the bank appear less profitable and riskier. Too little provisioning puts banks in a better light in the short term but can jeopardize financial stability in the long run if sufficient funds are not available to cover actual defaults.

What has changed about the disclosure of these LLPs for privately held banks?

While listed banks in Germany adhere to the stricter disclosure requirements of IFRS, privately-held banks were not required to disclose credit risk provisions transparently for a long time. Instead, they were permitted to report these credit losses within a broad and highly aggregated line item on the income statement. This allowed bank managers to use LLPs for opportunistic reporting practices, such as earnings smoothing. The implementation of the new EU Disclosure Regulation in Germany in 2008 and 2009 mandated that privately-held banks disclose their LLPs separately and in detail for the first time. Our study investigates the consequences of this increased transparency.

What were the results of these changes?

The study clearly demonstrates that bank managers required to disclose their accounting decisions are less likely to resort to opportunistic provisioning practices, particularly income smoothing. Specifically, they are now significantly less inclined to reduce LLPs to smooth income and increase a bank’s profits in the short term. The study also shows that the new disclosure requirements lead to provisions that better reflect future write-downs, making them much more predictive of future loan defaults. Additionally, the disclosure change shows real effects, with the quality of loan portfolios significantly improving around the increase in transparency. However, the response to the disclosure varied among banks, depending on the incentives of their respective stakeholders to use this new information. Banks with less secure funding and those located in regions with highly competitive information environments were more significantly affected by the change in transparency, prompting stronger adaptations of bank policies in these areas.

Simplified visualization of loan loss provisioning

Overall, disclosure means more financial stability

The study clearly demonstrates that transparency plays a decisive role in shaping the behavior of bank managers, even in privately-held banks. Transparency serves as a crucial tool for disciplining banks and positively impacting financial stability. Our findings suggest that stricter disclosure requirements for privately-held banks can enhance the monitoring efforts of market participants and local stakeholders, thereby disciplining banks’ risk-taking even in the absence of capital market demand for accounting information.

This change in bank policies, occurring without capital market pressure, underscores the important role of depositors and public scrutiny in monitoring and disciplining bank managers. Overall, transparency, through the comprehensive disclosure of information by banks, has a positive impact on financial stability and thus proves to be a useful tool for regulators.

To cite this blog:

Bischof, J. (2024, September). How Disclosure of Loan Loss Provisions Contributes to Financial Stability, TRR 266 Accounting for Transparency Blog. https://www.accounting-for-transparency.de/how-disclosure-of-loan-loss-provisions-contributes-to-financial-stability

Responses