Tax Complexity Index: 2022 data is now available

Researchers from the TRR 266 “Accounting for Transparency” at LMU Munich and Paderborn University publish the 2022 data of the Tax Complexity Index. With now four years available (2016, 2018, 2020, 2022), the data offers insights into the development of rapidly changing tax landscapes for multinational corporations (MNCs) around the globe. The data is available via open access on the interactive website www.taxcomplexity.org.

In recent years MNCs have faced increasing levels of tax complexity, making it an important aspect to consider. This development is shaped by, among other things, multiple trends in global tax systems, such as new regulations, digitalization and global tax competition, each of them with potentially ambivalent effects on tax complexity.

The Tax Complexity Index, developed by TRR 266 researchers, measures the complexity of a country’s corporate income tax system as faced by MNCs and is based on the Global MNC Tax Complexity survey. Since 2016 the survey is conducted every two years and answered by up to 1,000 tax consultants from up to 110 countries.

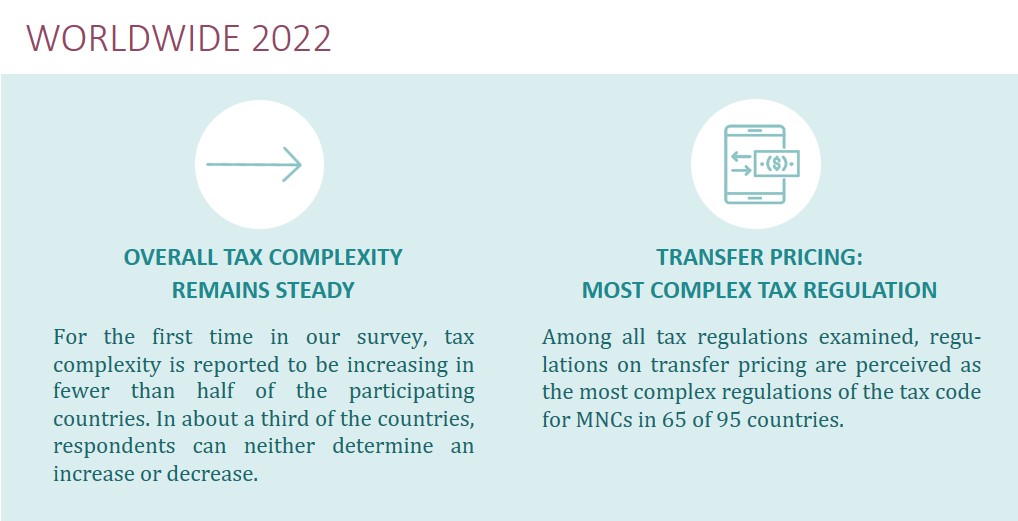

The now published 2022 data shows that the general level of tax complexity remains steady. This is a first since the start of the survey in 2016. Before, tax complexity has continually increased every two years. The findings also identified transfer pricing rules once again as the most complex tax regulation. In addition, the survey also examines tax processes. Thereby, we find that survey participants perceived inconsistent decisions by tax officers as the most serious problem in the tax audit process.

Compared to the previous surveys, the 2022 results indicate that a larger proportion of OECD countries perceive that tax complexity has only negative implications for MNCs and may be a factor for them to shift business activities abroad.

Detailed information and analyses of the results can be found in the Executive Summary of the 2022 survey and on our Global MNC Tax Complexity Survey webpage.

Interactive website

The newly collected data is now validated and openly available on the interactive website. The results are particularly interesting for policymakers, practitioners and researchers. With the data and our analyses we want to enhance the understanding of tax complexity in and across countries as well as developments over time. In addition to comparing individual countries, the website also offers a comparison of EU and OECD countries.