Unpacking Transparency: How it shapes organizations and markets

Transparency within organizations plays a pivotal role in modern economic systems. Defined as the quality of information shared and processed between senders and receivers, transparency can enhance decision-making, improve market efficiency, and mitigate information asymmetries. However, achieving transparency is often complex and comes with trade-offs.

The TRR 266 study “Accounting for Transparency: a Framework and Three Applications in Tax, Managerial, and Financial Accounting” by Jannis Bischof (University of Mannheim), Joachim Gassen (Humboldt University of Berlin), Anna Rohlfing-Bastian (Goethe University), Davud Rostam-Afschar (University of Mannheim), and Caren Sureth-Sloane (Paderborn University), published in the Schmalenbach Journal of Business Research, explores how transparency shapes organizations and markets. Using a novel sender-receiver framework, the study examines how transparency varies across contexts like taxation, managerial practices, and financial disclosures. The bottom line is transparency is context-specific, hard to achieve, and often has ambiguous consequences.

The Sender/Receiver Framework of Transparency

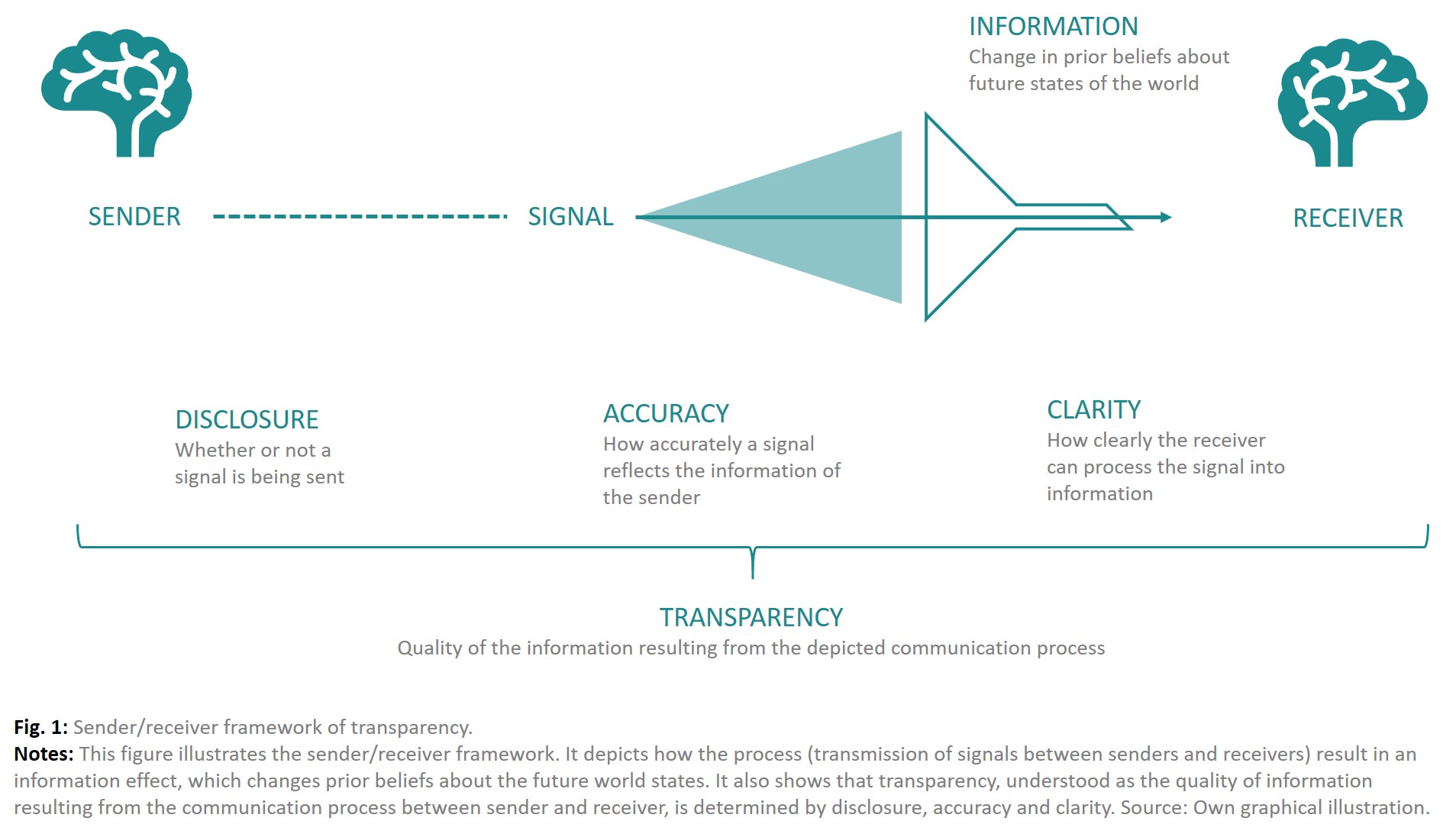

At the core of this study is the Sender/Receiver Framework, rooted in information science (e.g., Zins 2007), psychology (e.g., Schnackenberg and Tomlinson 2016), and economics (e.g., Arrow 1996). It defines transparency as the outcome of a communication process between the sender (the entity generating and sharing a signal) and the receiver (the entity interpreting and acting on that signal). The quality of the information resulting from this communication is determined by whether the signal is made available to the receiver, how precise or reliable it is, and how easily the receiver can understand and use it. The framework is illustrated in Figure 1 and breaks transparency into three key dimensions:

- Disclosure: Is the signal available and accessible to the intended audience?

- Accuracy: Does the signal precisely reflect the sender’s knowledge?

- Clarity: Can the receiver understand and act on the signal effectively?

Therefore, transparency is highly context-specific and depends on both the sender’s ability to provide signals and the receiver’s ability to process them.

Source: TRR 266 Accounting for Transparency

The researchers use three analyses to showcase their framework and the highly context-specific implications of transparency. First, exploiting novel survey data, they analyze how firms use tax literacy and tax advice in their strategies to cope with the complexity in tax regulations and thus navigate the lack of regulatory transparency. Second, they study the information asymmetries associated with working from home and how the design of working environments can mitigate them, thereby contributing to understanding transparency within firms. Third, they use survey data to analyze managers’ understanding of how financial statement users benefit from firm disclosures as a transparency device and how this understanding affects the managers’ assessments of disclosure regulation.

Transparency of Tax Regulations & Tax Knowledge

Firms invest in tax literacy (internal tax knowledge) and tax advice (external tax knowledge) to navigate complex tax regulations. Survey-based evidence from more than 800 firm decision-makers from the German Business Panel (GBP) of the TRR 266 Accounting for Transparency indicates that these two forms of tax knowledge often function as substitutes. Interestingly, firms that expect financial losses tend to rely more on external advice, highlighting how the firm’s economic context shapes the balance between internal and external tax knowledge.

Work-from-Home, Motivation, & Management Control

Hybrid work environments (mixing office and remote days) can provide an organizational solution to address transparency problems in working-from-home environments that hinder efficient incentive provisions for employees. They facilitate the within-firm exchange of information between employers and employees and thus provide enhanced within-firm transparency.

Disclosure Regulations

Managers are often critical of new disclosure regulations, such as the recent EU-wide adoption of the Sustainability Reporting Directive (CSRD), because of the substantial bureaucratic burden associated with increased disclosure requirements, i.e., releasing more signals. However, the support for those regulations increases significantly when managers are aware of the market-wide benefits of corporate disclosures, especially the facilitation of market transactions with receivers such as external investors, lenders, and suppliers. Survey evidence from the GBP showcases how managers deal with this trade-off.

Why does it matter?

Transparency is not a one-size-fits-all solution. Its impacts—ranging from improving decision-making to imposing regulatory costs—depend on nuanced sender-receiver interactions. This research offers valuable insights for policymakers, business leaders, and regulators seeking to design effective transparency-driven policies.

To explore the framework and findings in detail, read the article here.

To cite this blog: Bischof, J., Gassen, J., Rohlfing-Bastian, A., Rostam-Afschar, D., & Sureth-Sloane, C. (2025, January). Unpacking Transparency: How it shapes organizations and markets, TRR 266 Accounting for Transparency Blog. https://www.accounting-for-transparency.de/unpacking-transparency-how-it-shapes-organizations-and-markets/

Responses